Buckle Up

“It’s our dollar, and your problem” - The Fed

What a month. Despite the bear market, there is plenty to discuss. Bitcoin is ranging around 20k and all of the speculators have left town. All that remains are the diehards, and I’m proud to be one of them.

If you can’t handle the volatility, this asset class isn’t for you, and that’s okay. It’s brutal. You have to embrace the unknown, live in the grey, and bet on yourself.

I’m going to break this newsletter down into three parts: central bank digital currencies (CBDCs), macro recap, and Bitcoin news. They all tie together, and regarding CBDCs, it’s important you are at least aware of the term in the digital asset space and the potential implications.

CBDCs

What in the HELL is a CBDC???

It stands for Central Bank Digital Currency, and it’s LIKELY coming to a digital wallet near you in the next 5-10 years. It’s basically digital money right from the Federal Reserve to you. Your local bank would more or less be out of business. Nearly every country is experimenting with them in various fashions, some are ahead of others. China for example is WAY ahead of everyone. They are actively testing, and some citizens are using CBDCs for payments. Most other countries are in the heavy R&D phase but make no mistake, they are coming.

CBDCs are going to be insanely controversial (Yay! Something else to fight about!) over the ensuing years as they are all about CONTROL. Central banks want granular control over everything. It would make their lives much easier and their monetary policy more effective…hence China leading the way here. Instead of just raising interest rates globally, they could literally with a CBDC raise MY interest rate and keep yours lower. CBDCs theoretically can determine where people can spend money, how much, and when. CBDC money can “expire” after a certain amount of time. For example, “you have 2 weeks to spend X dollars on groceries only”. - The Fed.

CBDCs are dollars built on blockchain technology that allows centralized authorities extreme control over money (and thus people) for the good of the state. If inflation is spiraling out of control they can pull the levers much more easily with CBDCs than just manipulating interest rates like they do today. In addition, the transparency into the economy will be greater so that in theory major financial crises can be averted ahead of time. The other supposed added benefits of a US CBDC are improved financial inclusion, lower costs, cross-border payment facilitation, and keeping the USD as the undisputed world reserve currency.

The most important thing I can emphasize here is that blockchains and CBDCs ARE NOT “a replica”, “better than”, or “just like” Bitcoin. They have ZERO in common.

They are the antithesis of Bitcoin in many respects. They are built with properties focused on trust, control, censorship, and authority. The technology is closed source. There is no proof of work involved, it is purely proof of stake and simply an evolution of today’s digital fiat world. Those nearest the top have the most control and derive the most benefits. All rules are arbitrary and discretionary and can change. There would be no privacy regarding your transactions.

When you hear or read about CBDCs in the near future, think about these things. Ask yourself who is really benefiting from the technology. YES, there will be some benefits, mainly simplicity/convenience, and even monetary credits/stimulus in all likelihood. That will be tempting for sure.

For example, “if you agree to use CBDCs we’ll give you X dollars per month, for free.” Might be hard to say no to.

The trade-offs for that convenience, simplicity, and stimulus will be significant - your freedom to save and spend as you please. I’m not sure if that’s the “American” way, and there will be much debate. As it currently stands, I’m opposed to the technology, but we’ll see how it evolves. I’m highly skeptical, to say the least. In addition, I see it as a direct attack and response to Bitcoin and what it stands for. THIS is the fight that governments are starting to take to defend the current system. A new challenger (bitcoin) has arrived, it cannot be stopped, and thus a new opposing strategy must be developed to hopefully compete against it and pray that the general public chooses convenience over freedom. Time will tell. We each may/will have to choose. Don’t ignore this developing technology as it will certainly impact your life. Stay informed.

Macro recap

I’ve never been one for Netflix or reality TV shows. I know people get really engrossed in them and binge watch because they’re so captivating and addictive. That’s macro for me right now. I mean, it’s absolutely intoxicating what is going on in the world right now, especially in relation to how these events impact financial markets, including Bitcoin/crypto. It all comes down to the underlying thesis and value proposition of Bitcoin: when backed into a corner and faced with difficult decisions, governments and central banks will ultimately resort to printing unlimited fiat to save/protect the status quo, devaluing your hard-earned income (and time). When that strategy ultimately blows up in their face is the question, not if. The timing is the hard part to predict.

UK pension fund crisis

This past week the entire UK pension system juuuuust about went insolvent. Can you imagine that? Everyone in the UK relying on a pension for retirement...trusting it will be there for them…poof. Gone. How did this happen? The short version in my opinion is that the pension funds in the UK were basically functioning like the Luna cryptocurrency Ponzi scheme that collapsed (but no government came to bail out). Pension funds were using cash to buy Gilts (UK bonds) and then pledging those Gilts as collateral to raise cash to buy more Gilts. This is called massive leverage and is super dangerous, but they “had” to do it in order to pay out the guaranteed pension plan returns since the Gilt market before now was so pathetic and provided zero returns. Since bond yields have only fallen since the 1980s (which means bond prices/value/demand is up) it was assumed they could never go up. Well, they did, and fast.

Because the US federal government is hiking due to inflation, every other country has to hike interest rates to match them or risk a massive currency devaluation (money flocks to the highest interest rate). In addition, the energy shortage and geopolitical crisis are causing the value of the USD to rise in comparison to other currencies (people need dollars in crisis). Even with foreign central bank interest rate hiking, it’s usually still not enough (see the Euro now at parity with the dollar).

When inflation is high and federal interest rates go up, short-term bonds sell off because investors want to be compensated for this. It’s an inverse relationship. Lower bond demand/lower value/price = higher yields. High demand/higher value/price = lower yields.

If you’re holding a 2-year bond at 0.15% yield and inflation is at 10% - that’s a raw deal. Bonds sell-off. When the government hikes rates and is now offering .75% yield and you’re still collecting .15% - that’s a raw deal. Bonds sell-off and bond YIELDS rise while their value falls.

In addition, the new PM of the UK announced plans for unfunded tax cuts and fiscal spending to revive the economy. Spend money you don’t have…everyone else is doing it, right? So should we! This was in DIRECT contrast to the Bank of England (BoE) RAISING interest rates to slow demand and inflation. Loose fiscal policy contrasting tight monetary policy.

Well, the financial markets weren’t too happy with that plan given inflation is at 10% in the UK and the war is sending Europe into a DEEP recession given the energy crisis looming larger by the day. The markets responded to this as a “policy error” and bonds (Gilts) and the British Pound sold off and yields skyrocketed.

No one wanted to be buying or holding the debt (bonds/Gilts) of the UK to finance their spending spree when they didn’t have the money to pay for it and inflation is high.

Back to the pension funds, their Gilts were being used as collateral in a highly levered strategy, and when the value of those Gilts tanked when bonds sold off …

Margin call time. Pension funds were asked to post MORE collateral/funds to stay solvent, and in order to do so, they had to sell assets to meet those margin calls. What did they have to sell? Stocks and Gilts. You see the death spiral here? Bond yields rise due to high inflation, monetary policy, loose fiscal policy, energy crisis, strong dollar – Gilt value falls – pension funds now have to sell Gilts to meet margin calls – Gilt yields rise as more and more are sold, etc. etc.

At that point, someone put up the Batman signal because they were screwed.

It was GAME OVER. Just like the Luna Ponzi when it started its death spiral, it unwound fast until it was worthless. BUT! Just like every other time in the history of fiat, mum and dad stepped in to save the day. Money printer…ENGAGE!!

The BoE bought 60 b-b-b-billion dollars of Gilts to stabilize the market. Where’d that money come from? A keystroke on a computer. Voila! Money! Can I have some too if it’s that easy?!?

They are also pledging to buy Gilts until mid October to stabilize the situation. If it ends there I’ll be surprised. Gilt yields are back on the rise. The market is testing them since they have offered to be the buyer of last resort.

The fact of the matter is that we no longer live (and haven’t for a looong time) in a free market. Everything is manipulated and certain entities are deemed “too big to fail”. They take risks that go against them and are bailed out. How is that fair? If you did the same thing tomorrow you’d be bankrupt and there would be no savior.

The government and central banks when faced with hard decisions will resort to unlimited currency debasement. Example # too many to count.

Bitcoin is a hedge against this.

European Central Bank (ECB)

The UK grabbed the headlines this week, but the ECB is in even more trouble long term. They are trying to manage interest rates for the entire Eurozone. Good luck with that! Some countries like the PIGS (Portugal, Italy, Greece, Spain) are badly in debt, while others like Germany (until recently) are in solid shape. It’s impossible to have a one size fits all policy amongst different countries that import/export different things and have different economies. The energy war with Russia is really going to test and exacerbate this problem. To protect certain countries from a sovereign debt crisis (like Italy), the ECB has proposed a new policy called TPI (Transmission Protection Instrument)…aka anti-fragmentation tool… "aka quantitative easing (QE) but we’re not going to call it QE so nobody yells at us”.

How it works is that the ECB will be the buyer of last resort for anyone selling off Italian bonds when their currency is in crisis given the tsunami of debt they have and the impending energy crisis they face. Oh yea, Russia just turned off their oil supply as well.

What will be the outcome here? Begins with a B and ends with an R. You say it when you’re cold.

Bitcoin is a hedge against this.

Japan

Japan gets the nod here as the worst with a QE policy that is on a roid’ rager and then some. They’ve been doing QE for decades to save their bond market, but things are getting heated/accelerating now. They are buying all the bonds to defend the bond yield of 0.25%. If bond yields go above that they will print unlimited amounts of money to buy bonds to defend that yield. If bond yields go above that they will be insolvent quickly given how massive their debt is (debt/GDP = 260%), but who’s counting?

The problem with this strategy is that now the Fed is raising interest rates. That’s causing Japanese bond holders to sell their bonds and the Yen they get for them to go buy US bonds with higher rates. This has led to massive QE AND massive devaluation of the Japanese Yen as people ditch the Yen to buy US dollars.

Japan as a result now is forced to sell US bonds to “defend the Yen”. This means they are selling dollars/US bonds to buy Japanese Yen to stabilize the price and prevent it from crashing. This puts pressure on US bonds because bond selling = higher yields. Higher yields = debt is more expensive to repay. Death spiral type stuff again - this time for the US if they don’t step in at some point and lower bond yields. That hasn’t happened yet, but if it did the US bond market would devolve into pure chaos. I think it’s going to happen in my lifetime. It’s brutal out there. Every country for themselves.

Bitcoin is a hedge against this.

Russia

Too much to even try to write about fully. Russia thinks it’s winning, but evidence says to the contrary. Via sham referendums, they are trying to annex parts of Ukraine that they temporarily had control over. Ukraine is battling back and winning ground. This is good, but concerning. I say that because Putin is a maniacal dictator. He can’t tolerate losing. He is ALL IN. This war is everything to him. He has no exit strategy. I fear escalation including nuclear warfare and significant US involvement at that point. I hope I’m wrong but Putin isn’t going to exit nicely.

Importantly, Nordstream 1 and 2 oil pipelines were blown up this past week. This is like 2 planes flying into the WTC. Pure acts of war. It makes sense because as we discussed – it’s an energy/currency war. We have no clue who did it, but it basically takes a compromise off the table for Europe. They can’t bargain with Russia for oil/gas this winter if the pipelines that send it to them are destroyed. Russia’s leverage is gone and Europe also panics without energy.

Who stands to benefit from this?

Gotta love a good conspiracy theory! Our energy exports will benefit for sure.

China

Who knows to be honest. There is no reliable information that comes out of there. They seem to be stuck on a zero covid policy which is still crippling supply chains. They also seem to be in the midst of a massive housing crisis. They keep toying about invading Taiwan. You won’t know about a problem there until it’s readily evident to the entire world given how they cover up information. The end.

America

What is going on with the American economy is SUPER complicated in my opinion. There are so many cross currents that it is impossible to make any solid predictions. There are lots of people calling for a 2008 GFC crash and just as many others stating that the American economy is strong. Thus, the answer probably resides somewhere in the middle – no crash, but not robust growth. Maybe/likely a bit more downside to come this winter. There is conflicting evidence everywhere.

For example, housing prices are starting to fall but higher interest rates are preventing people from selling, thus limiting available supply and keeping prices elevated. Overall housing supply is on the low side historically as well.

Jobless claims are rising but there is a massive number of jobs still open given the workforce shortage and resulting higher wages, which gives people more options/bargaining power.

Inflation is high but is peaking and rolling over with supply chain pressures easing, gas prices falling, and high inventory levels causing markdowns.

Inflation could just as easily start going back up though with OPEC+ cutting oil supplies and the SPR drain ending in late October sending gas prices back up which sends prices for everything back up. Wages also keep going up with the workforce shortage keeping CPI elevated.

Americans have record amounts of cash in reserves from the stimulus checks handed out during the pandemic, but they have now really eaten into those reserves due to inflation, and credit card usage/debt is back to all-time highs.

Interest rates have gone from 0 to 3% insanely fast

but MAY start slowing given the global destruction a strong dollar has with rising interest rates (see UK pensions above). In addition, the US debt just surpassed 31 t-t-t-trillion dollars. A new record, bravo!

Higher interest rates on 31 trillion dollars of debt is completely unsustainable, and thus they should come down in the future. The debt increase will start to compound/go exponential as interest rates/yields are now higher. This will bring higher yields and a faster debt spiral.

Finally, even though inflation has caused prices to go up, this in the short term actually benefits the government as higher prices mean higher taxes collected (income, sales, property, etc.). It also allows them to monetize the debt as dollars are worth less with high inflation. The problem is that the cure for high inflation is inflation itself. We are seeing that now where eventually the consumer is tapped out and can’t pay for discretionary items because they spend all their money on food and shelter so the economy goes into the tank. Recession ensues. When a recession hits tax collections go down because people are making and spending less and the stock market nukes. Less taxes = less ability to pay the debt on 31 trillion. Solution? Raise taxes. JK. Money printer – ENGAGE.

See all the counter currents out there? It’s nuts! Ultimately, the Fed is going to keep raising rates and slowing demand for goods and services, and crushing the labor market as that is their only tool in the tool belt to fight inflation.

They’ll stop when something breaks. Is that a US pension fund? The bond market? A large G-7 nation economy that is an ally? I’m not sure.

The US economy is resilient. The rest of the world is not given the war and energy crisis. Regardless, we are all connected. All I know is that there are major tremors underneath the surface. Avoiding a big financial earthquake calamity is becoming increasingly difficult.

What will ultimately be the end result for each country? Monetary debasement. Forever and always when push comes to shove to “save the system”. The system is broken. It is past the point of repair. You have to participate in it and use it in order to function in daily life (pay bills, etc.), but now there is finally a way to opt-out.

Bitcoin

A few things about bitcoin the asset and bitcoin the monetary protocol to finish up.

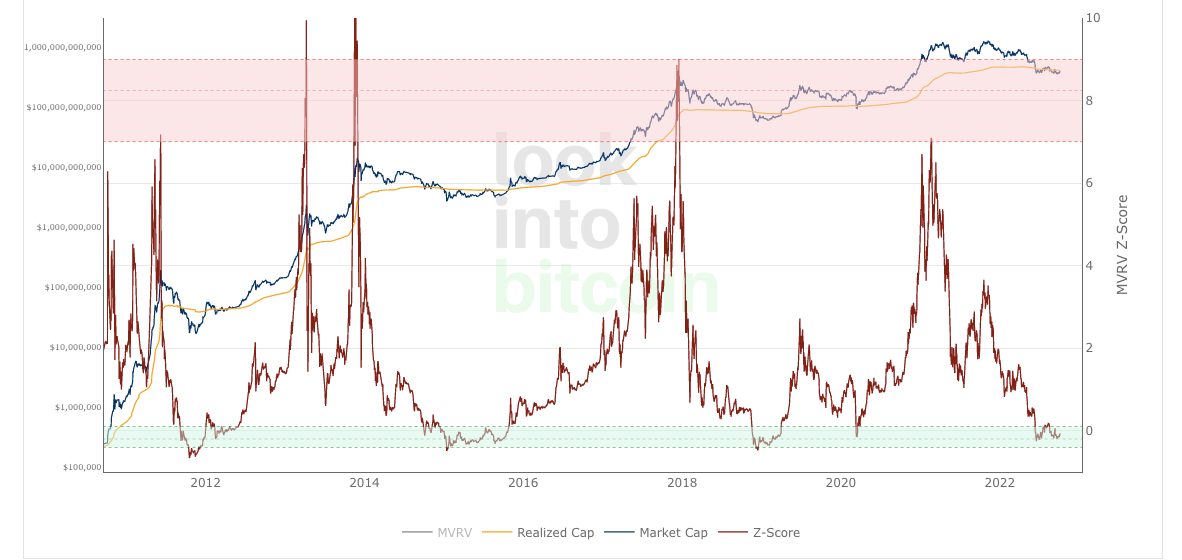

BTC the asset is range bound and stays at historic value territory.

My gut tells me there may be another leg down this winter given the tremors discussed above and WWIII escalation. Nothing will be safe in that scenario (except cash). For that reason, I’m just pursuing my DCA strategy and have a chunk of cash ready to deploy if we get that leg down. If it never happens, so be it. Stacking sats either way.

Importantly, you always need to look at the health of the network and ignore the asset price. The price will vary widely given macro issues, but if you look under the hood you’ll find if your investment thesis is on track. For Bitcoin, it’s all about miner hashrate (security), new users (demand), and scaling applications (growth). Miner hashrate just hit an all-time high the other day, IN A BEAR MARKET.

That means people/companies/nation states all want in on the action. You love to see it. Unlike with ANY OTHER ASSET ON THE PLANET, an increase in demand DOES NOT come with an increase in supply. For example, when gold prices go up that encourages gold miners to dig more up and sell it for profit. What happens? More supply leads to falling prices eventually. With Bitcoin, the difficulty adjustment prevents that. The difficulty adjustment JUST WENT UP because the miner hashrate just hit an all-time high. As more miners try to acquire bitcoin, it just gets harder so that the issuance stays near constant. Please understand the significance of this. It has never existed before in human history. Proof of work and the difficulty adjustment are the 2 most profound inventions of our time. We’ll all be dead before it’s fully appreciated, just like with many other significant inventions in history.

New users continue to grow despite the bear market.

Exactly what you want to see. More users = more demand = more growth with limited supply = number go up. Whether you’re using the bitcoin monetary protocol as a pure store of value to escape the current fiat system, using it as a medium of exchange in a developing country to buy things, building a business to disrupt the entrenched oligopolistic payment networks, or building a bitcoin mining center to take advantage of and incentivize cheap renewable energy sources, it really doesn’t matter. These are all things that add value to the bitcoin network and bitcoin the asset itself, and those are just a few of the examples out there. The bitcoin network is an OPEN network. That means that anyone in the world can tap into and add value unlike a closed network (ex. Meta, Apple). It’s like “owning” a piece of the internet and whenever ANYONE in the world adds something of value to the internet your piece of ownership of the internet goes up in value.

That brings us to bitcoin scaling technologies. Bitcoin needs to scale for the 8 billion people on the planet to use it. It’s in the early stages right now but the Lightning network is doing just that, and at an exponential pace, despite the bear market.

The alpha release of Taro came out the other week and I think this will be bitcoin’s mainstream moment when it’s time.

Taro will allow users to transact stablecoins like USDC, Tether, etc. on the Bitcoin lightning network (see prior newsletter related to the Lightning network built on Bitcoin if you missed it). People don’t want to spend bitcoin because it’s still in its store of value phase of becoming money. You don’t spend something that is going up in value. Let alone the taxes you pay when you spend it in this current regulatory environment. Thus, you HODL bitcoin. BUT, you DO want to spend DOLLARS in everyday life and that’s exactly what Taro (using Lightning) will allow. Transacting digital dollars/stablecoins ON the bitcoin lightning network without ever spending your bitcoin or paying taxes (because you’re transacting dollars). This technology allows you to use the bitcoin open monetary network as a payment rail but never requires you to hold bitcoin the asset if you don’t want to.

The reason why you would choose to do this is because of the fees and simplicity. Since bitcoin is an open network, it doesn’t need to take a cut like Visa, Mastercard, and others do. They are businesses that report to their shareholders and must make a profit. Bitcoin don’t care about profits or shareholders, it’s a protocol. So, if you’re a merchant and someone can transmit dollars to you over a free and open monetary network and you no longer have to pay the credit card company a fee, that’s huge! Also, merchants can LOWER prices for consumers since they don’t have to pay that fee = more business = everyone wins. Except for the closed payment networks. What you use and love today will likely not exist in 10-50 years. Paypal, Venmo, Visa, Discover…goodbye. Crazy, right? Just like Blockbuster when a new technology comes along and disrupts everything. Adapt or die. Keep an eye on this development. Undeniably positive real-world use cases, especially during times of high inflation when people are looking to cut costs, will be the tipping point for bitcoin.

Until next time…buckle up out there.

Thanks for reading!

THIS is Crypto Pulse