The Show Goes On!!

The Show Goes On!!

Debt ceiling drama and other rumblings

The party at the White House after the debt ceiling deal was signed…

I’m back, baby!

Sorry for the layoff. Took some time off writing for paternity leave, work, and a golf trip (shoutout to my amazing wife), but I never took a day off learning/studying bitcoin!

It’s been a brutal bear market and not a ton is going on, but there are some noteworthy things to discuss, so let’s get to it.

More banks failing

Since the last newsletter, a few more banks failed. That brings us to a total of six since the start of the banking crisis.

That’s certainly not a “nothing burger,” if you ask me. Compare it to 2008 (graphic not even up to date with all six!).

Banks are supposed to be “safe” investments. A “safe” place to store your money. Maybe not. Maybe this bitcoin thing isn’t so volatile and risky after all compared to investing and saving your hard-earned dollars in a bank. Who would have guessed that 10 years ago?

Bitcoin as a cyberspace bank account where you store your wealth in a fixed supply scarce digital asset, backed by energy, with no counterparty risk, turns out to be a hell of an invention! Technology for the win!

Unfortunately, for smaller regional banks, I don’t think the pain is over.

We’re in the eye of the storm, similar to when Bear Sterns collapsed in 3/2008, and everything seemed hunky dory for six or so months until Lehamn Brothers went bankrupt in 9/2008. I’m not saying the timeframe or outcome will be the same, but there are some dark clouds ahead. Two in particular.

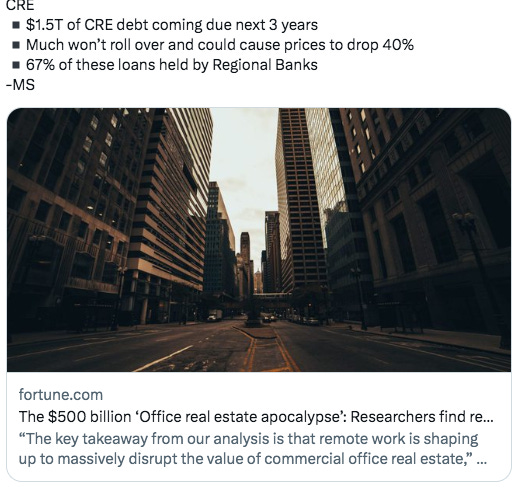

First: Commercial real estate implosion– If you’ve been reading this newsletter for any amount of time, you know I’ve been shouting this from the rooftops. I was doing it BEFORE it became mainstream (humble brag) and will continue to beat the drum. The best word to describe it is apocalyptical.

Covid permanently changed how Americans work. Work from home is NEVER going away. The 9-5 office job five days a week in the city is done. There will likely be some degree of hybrid work, but we’re never going back to the 2019 office routine.

Everyone knows the show “The Office.”

Part of the reason the show was so funny and popular was because everyone hated their job working in an office. During covid, people got a taste of working from home, were similarly productive, saved money, and for many – were much happier. Employers can’t take that away, especially given the current labor shortage, and employees are demanding it. Add on top of that what Apple just released – the Apple Vision Pro

along with the Quest AR/VR headset (by Meta), and I believe the transition to work from home will only accelerate over the next 10 years. You may think AR/VR is dumb now, but it will iterate and get cheaper, faster, smaller, and sleeker to the point everyone has one, and it becomes as ubiquitous as a smartphone in your life. We are living through a massive societal change in how humans work, and the ramifications are enormous (and mostly unknown).

One ramification I know for sure is that a massive chunk of office space is now worth ZERO. Zero. Especially class B/C office space that hasn’t been renovated since the 1980s – you know the ones. These buildings are massive and worth millions (sometimes billions) of dollars. Owners need tenants to lease the office space and pay rent. That’s how they repay the bank loan they took to build the office building. NO ONE ever thought office buildings would no longer be necessary. It has always been a stable and rock-solid investment for big funds like pensions, etc. Guaranteed steady cash flows as Americans head to work every day to work for the man. Welp, they were wrong.

Just like Blockbuster thought Netflix and streaming was a fad and Kodak thought digital pictures would hurt their business model, the pain train is coming fast as technology disrupts the traditional work model, and that’s big trouble for regional banks.

A recurring theme you’ll hear me talk about that Jeff Booth emphasizes in his book (The Price of Tomorrow) is that technology dematerializes and disrupts nearly everything in our lives, making it cheaper, faster, and generally better (with some debate). Zoom and Microsoft Teams, using the internet and high-quality broadband networks (all technologies), destroyed the need for office buildings seemingly overnight once Covid hit. You would have never thought that was possible in 2000 using dial-up internet and AOL, but just 20 years later, we are looking at MASSIVE disruption that is profoundly deflationary.

Tenants are not renewing their leases at staggering rates. They are saving money not paying rent and their employees are happier – a no brainer decision. Building owners typically have 5-10 year loans with variable interest rates, and starting soon, will need to refinance at rates north of 6% with fewer tenants and higher insurance costs. Many will hand the keys back to the bank that provided the original loan and say, “Sorry, I can’t pay it.” The bank is then on the hook, and a vast majority of commercial real estate loans are via small regional banks.

Suddenly, bank balance sheets with bad CRE loan debt start to look bad, and bank runs start all over again, similar to how SVB collapsed so quickly when their balance sheet was exposed. And I’m not even including the massive bond losses many small banks have already sustained given the rapid rise in interest rates (the primary reason SVB failed).

Importantly, and what the Fed didn’t anticipate before with SVB, is the speed at which a bank run can happen. In the 1930s, you had to run to the bank to take out your money physically. It was a lengthy, slow process. Today? Tap tap tap on your phone and it’s done in a few seconds. Once again, technology dematerializing and disrupting everything in our lives, including banks.

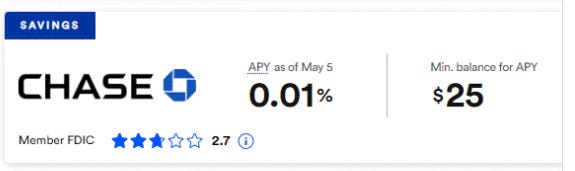

Second: The slow bank walk – as opposed to a bank run that happens over a day or two, the bank walk is happening slowly but persistently. Each and every day people are waking up to the fact that their bank is offering them < 1% APY

on their savings and they can instead move their money to Treasury bills or money market funds and earn 4-5%. A massive difference. If you aren’t doing this yourself, I implore you to get on it quickly as you’re just leaving free money on the table.

As people slowly and methodically walk their money to these non-bank sources of yield (I use Robinhood earning 4.65%), banks come under stress.

Banks NEED our deposits to make loans and earn a profit. That’s how they operate. You deposit your money, they loan it out with interest and give you a small cut for your service. The problem is that they’re not giving us any of the returns (<1% interest) and are keeping the profits basically all to themselves. Unfortunately for them, if they raised rates to prevent people like me from moving my money out, they’d go bankrupt from having to pay out more interest to their customers. It’s a toxic situation and will eventually lead to more bank failures as their balance sheet shrinks, bad CRE loans accumulate, and fewer loans are made in a high-interest rate environment where nobody wants to take out a loan at 5-8%.

Just because banks aren’t failing every day in the news now doesn’t mean it’s not ugly under the hood. The BTFP program (created in March) is getting tapped more and more every week - that is BAD NEWS.

Banks only should use that when they’re in distress. Something sinister is happening beneath the surface, we just don’t know what/when the next crisis will be.

How do I invest to capitalize on this prediction? For a while, I contemplated shorting/buying puts on banks and CRE-focused equities. The problem is that it’s not easy to do, and the stock market is ridiculously manipulated, so it’s easy to get hurt with these strategies. Instead, I just buy bitcoin.

The more I learn and the deeper I go with bitcoin the more I realize it’s the simplest answer to everything with the least risk. More banks will fail for the reasons discussed above. The guaranteed, no doubt about it, 100% certainty, bet your life on it response by the Fed will be to bail them out. Bail in vs. bailout? I don’t give a damn what actually occurs. It’s money printing in some form or another at the end of the day. Banks win, we all lose. The show goes on. Print more money to make the problem temporarily go away.

Bitcoin is becoming the most scarce and desirable asset on the planet. The more they print, the more fiat will find its way into bitcoin, and there’s only 21 million. The USD has a supply of infinity. Read that again….infinity. Your options are to take your current and future wealth and divide it by infinity, or divide it by 21 million.

Replace “Euro” with “USD” or ANY other fiat currency:

It’s not rocket science folks. It’s so simple people can’t even believe it’s real, but it is, and I’m trying to open your eyes to it now to protect your wealth and ultimately your time on this earth. Time is money, and it’s the only thing more scarce and valuable on this planet than bitcoin.

The debt ceiling passes!

Ah the Kabuki theater. Such drama. Bravo! What a show. Encore! Encore!

If you thought for one millisecond they weren’t going to raise the debt ceiling in time…we need to talk. The theatrics are truly mesmerizing, but at the end of the day, it’s just a show, and you’re paying for it.

Importantly, NOTHING WAS SOLVED. NOTHING.

They did what they always do and will always do. They kicked the can down the road two years so we can all go to the show again! Encore!

Look at history. You thought this time was going to be different???

The same script will play out in 2025 and they’ll raise the roof then too at the last minute. The US is 31 trillion dollars in debt, and with higher interest rates on deck for our new debt issued at ~5% that number will grow fast.

Nearly the entire annual tax revenue budget goes to defense, social security, medicare, Medicaid, and interest expenses. Which one of those things do you want to cut? Yea, no good options are there? Thus, congress puts more on the credit card to keep the party going and raises the imaginary debt ceiling so we can all pretend like this time is different and we’ll be more fiscally responsible.

Here’s the problem the US and much of the world faces – demographics are destiny, and there is no calvary (young people) coming to the rescue like with the baby boomer generation.

More young people = more jobs, spending, and tax revenue. That was the recipe for our monetary system's success, but those days are fading fast.

Now we just have an aging population that lives longer/works less and spends less as they age, is more unhealthy, needs more government handouts, and on top of that we’re facing a likely recession where both young and old people alike will lose their jobs and consequently spend less (= less taxes collected). That’s a bad recipe for our national debt, if you ask me.

Why not just raise taxes? Easy right? Last I checked, it’s certainly not easy to get elected or re-elected by campaigning for higher taxes. In addition, the top 25% of income earners already pay 90% of all taxes collected. You can try and squeeze the rich some more, but eventually, they leave and bring their wealth (and the jobs they create) with them. It’s not a simple solution. So what are the options?

The only way out of this mess is three things (and what would be the likely result):

1) Default on the debt – the world would burn down. War. Mad Max scenario type stuff when people don’t get paid what they’re owed/promised. Pure chaos.

2) Fiscal responsibility – massively cut spending, higher taxes. Severe depression and life is brutal for a decade or so. Americans can’t tolerate pain like this in 2023.

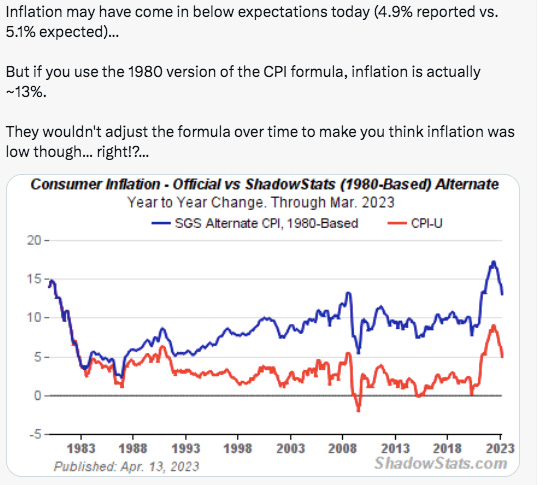

3) Debase the currency to infinity and inflate the debt away – anyone holding dollars is a frog in a slowly boiling pot of water completely oblivious to their purchasing power being inflated away (but at least there’s no anarchy in the streets!). The rich get richer. Inequality widens. The show goes on. If you’re lucky and rich enough to invest in stocks, you barely keep pace with inflation even with 8% returns, mostly because CPI is a manipulated number and is actually much higher than reported.

Life just seems to get slowly harder where a 100K salary doesn’t mean what it used to. Depressing, huh?

How do I invest to capitalize on this prediction? Shocker! I buy bitcoin.

There has never been an option OUTSIDE the inflationary fiat system we use until bitcoin came along in 2009. It was the purpose of bitcoin. A MAN-MADE technology that disrupts the legacy system. Just like the internet, this is a MASSIVELY disruptive technology that is going to change the world in ways we can’t even imagine.

Humans literally invented perfect money. How awesome is that??!! We don’t need a shiny gold rock anymore, just like we don’t need Rand McNally maps when we have Google. Just like you couldn’t imagine Uber on your phone when you were chatting in an AOL chat room back in the day, you can’t even begin to comprehend a bitcoin world. It is coming though, and fast. Companies are integrating and building with it as we speak.

Every time they raise the debt ceiling and kick the can bitcoin grows stronger. The raised debt ceiling is great for bitcoin, don’t second guess it.

And remember, when they stare you in the face on TV and say, “We averted a crisis and solved the problem,” what they really are saying is, “We are pathetic and weak. We can’t balance our budget like we require every American citizen to do. We’ll keep spending money we don’t have and dump this on our kids to figure out, but we’ll be dead so the joke’s on them. Godspeed.”

I can’t look my kids in the eyes knowing there is a problem but just stand aside, shrug my shoulders, and cross my fingers for them. Especially when I truly believe the solution is staring us right in the face. A return to sound money built for the digital age. Sound money that moves at the speed of light and streams like music. Sound money that no one controls and manipulates to their benefit.

The Presidential Election

I honestly didn’t think it would be on the ballot in 2024. I told my parents that in 2028 a legitimate candidate for President of the United States would support bitcoin, and possibly win. As of a few weeks ago, there are now three candidates who are openly pro-bitcoin. DeSantis, RFK Jr., and Ramaswamy.

Bonkers. All three are actively talking about it and I believe come next year bitcoin will have some say in who wins the primaries and, ultimately, the Presidential election. Bitcoin is a massive draw for moderates like me. Hardcore Republicans and Democrats will vote along party lines no matter what, and that’s fine. But I’m a single issue voter, as will be millions of other bitcoiners, and that could sway things. Bitcoin is now on the ballot. I don’t like politics as I think it’s all theater. I believe the money is broken, and nearly everything that is broken and corrupt in society today stems from that. Fix the money, fix the world is my motto. If a candidate opposes bitcoin, I cannot/will not vote for them because in my mind they oppose freedom, and that’s anti-American. If they’re concerned about energy waste, that means they’re just uneducated and haven’t put in the work to understand it. A major red flag.

The great thing about bitcoin is that it doesn’t run along a party line. It doesn’t care – it’s a protocol. It’s just math and code and can’t be influenced. Bitcoin changes you, you can’t change bitcoin. That’s the beauty of it. Whether you’re a Republican or a Democrat or something in-between like me, bitcoin is for you. It has something for everyone, and that gives me a lot of hope for once related to politics.

.

The economy

Your guess is as good as mine what will happen with the economy. Rate hikes usually hit with a lag of 12-18 months, and the first rate hike was in March 2022, so we’re now getting into the thick of it, and the Fed still may raise rates again in June/July…

…a mistake, I still think. There are just as many reasons to think the economy is going into recession as there are reasons to think everything will be just fine. Some analysts think a nasty recession is coming in Q4 or Q1 2024. I tend to think they’re right, but the stock market is forward-looking and may have “already priced that in” to some degree, and now is heading higher off the October lows. I’m not sure. I can’t wrap my head around the housing market and interest rates at 7-8%. No one is buying, and no one is selling. It’s a standoff. But the economy runs on the housing market, and if that is stagnant, then everything falls apart. However, jobs are plentiful, wages have increased, and stimmies from Covid handouts still resonate throughout the economy. For example…

Student loan payments will finally restart on 9/1/23. That has been a significant stimulus for many, including myself, and it’s just now going away. I think we’ll see the effects of this later in 2023, or early 2024, but it’s impossible to know. If the economy does great – bitcoin will chug along. If a nasty recession hits, bitcoin will sell off with everything and then go to the moon when they turn back on the printer. Win-win as I see it. My strategy? DCA and chill.

More importantly….

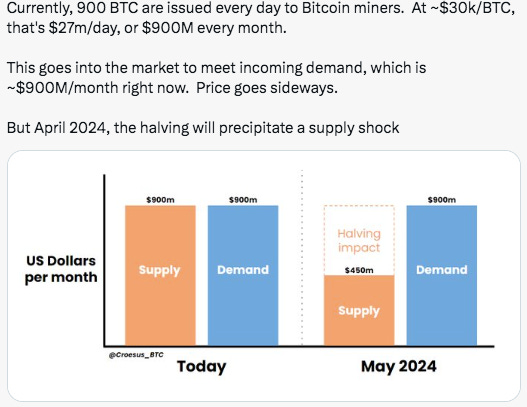

The bitcoin halving is next spring, 2024, and that’s incredibly bullish (especially when Presidential candidates will be talking about it non-stop in the fall). The reason the halving forces the price higher is because overnight, the cost of production doubles. Miners spending ~$20,000 to mine one bitcoin now have to spend $40,000 to get the same amount as the supply gets cut in half.

There is no other commodity on the planet where this occurs, and you can guarantee that the cost of production will only rise into the future as the block reward shrinks programmatically every four years. Bitcoin miners typically won’t sell their bitcoin at a loss (duh, it’s a business for them), so the price moves higher, and a new equilibrium is established every 4 years. As price moves higher, FOMO and greed kick in, and given bitcoin’s scarcity, prices can shoot higher quickly and get out of touch with reality. For now, and leading up to the halving, I think the best strategy is DCA and chill, as Bitcoin is currently in good value territory but not a bargain like it was in January.

AI

I couldn’t help myself from discussing some AI stuff.

Nobody knows what the future holds, but my goodness, this technology seems powerful. The iterations are coming at lightspeed and will likely only get faster from here…buckle up.

Right now, to the common man, it may seem quirky and a luxury item, like asking Chat GPT to answer some questions for you or help you with some homework, but in the next 10-20 years, we’ll see some awe-inspiring things that integrate into our lives as slick as the iPhone.

How do I invest to capitalize on this prediction? Take one guess! I buy bitcoin. Sure, you could buy Apple, Google, Nivida, Microsoft, Meta, etc. Those companies are all double the bitcoin market cap and are at very mature stages and insanely overvalued due to the stock market run big tech companies have had in 2023. Bitcoin, on the other hand, is currently fairly valued, has a smaller market cap, a MUCH larger total addressable market, and is a bet on the disruption AI will bring to the job market and the profound DEFLATIONARY effects it will have.

.

AI (I believe) will necessitate an insane amount of money printing (from the loss of jobs and tax revenue) to create inflation and sustain the modern fiat Ponzi scheme we all use today.

Yes, I know we have INFLATION as we speak, but that’s no surprise when you shut down the world for 2 years and pump it full of printed money for people to spend while supply chains are totally wrecked due to lockdowns. What’s 7 trillion among friends?

Supply chains are now back to normal basically, free money is over (for now), and inflation is in free fall. I still predict we’ll see <2% CPI by 1/2024. Maybe not 0% as I predicted last December, but let’s wait and see.

We’re rapidly transitioning back to the defacto state of deflation that technology forces upon us. Everything it touches makes it cheaper, faster, and usually better. AI is going to create many jobs, but is also going to obliterate likely many more. Millions and millions of people are going to be competing with AI for a job over the next decade and I got news for you. AI costs less, works 24/7, doesn’t complain, doesn’t make mistakes, and doesn’t need health insurance.

The past 2 decades were so deflationary because of increased global trade, shipping cheap labor to China, and the plethora of US natural gas making energy cheap and plentiful. AI will make that 10xs worse as humans slowly get replaced and we tap into new energy sources while still using hydrocarbons.

As a doctor, I’m not immune to this disruption either. Imagine in 10-20 years a hospital preferring to pay a nurse practitioner half my salary, but they are augmented with AI using the Apple Vision Pro, and outcomes are equal, if not better. From what I’ve already seen, the technology is close to being ready to make this a reality. The culture change will be the slow part, but it is inevitable in my opinion.

Brace yourselves. Doctors, lawyers, computer programmers, and anyone sitting behind a computer for most of the day should be prepared for a pink slip. White collar jobs are the ones most at risk, but when AI merges with robotics, blue-collar jobs are on the chopping block next. No one is safe over the next 10-30 years.

.

This is deflationary. Profoundly. All of it. The cost of everything when AI and robotics are running the show basically goes to zero. Imagine taking a plane trip someplace. Why should the cost not be near free when AI flies the plane (it basically does 99% currently), robots transfer your luggage, offer you a soda and some peanuts, and get you through TSA and check you in? Think about that. Almost all the jobs that drive flying costs higher are due to humans. That’s not even considering 3D printing and building a cheaper, faster, lighter plane (also using AI and robotics) that uses less gas! Fly from New York to London for $100 bucks!

Technology is incredible. We should embrace it and celebrate it. Compare the life you live today to a life in 1920. The common things you take for granted today didn’t exist, or only the filthy rich could afford back then. Now almost everyone has a smart home, car (with Bluetooth), smartphone, computer, smart appliances, smart flat screen TV, grocery delivery service, Amazon deliveries, and can fly anywhere in the world in a day, etc. etc. During this decade many will get a college education for free on the internet in conjunction with AI that will be far superior to many traditional college offerings. Technology is disruptive, and it makes things cheaper and abundant. It is profoundly deflationary and is in direct competition with our inflationary fiat monetary system.

Technology will not stop advancing, and people’s lives will be improved. But in order to enjoy the benefits of technology, the inflationary debt-based system we use today won’t work. Technology brings deflation, and our current system requires inflation. One will win. I’m betting technology wins, and bitcoin (as a new technology) is a better money for that world where technology enhances our lives and brings costs DOWN, not artificially up due to an inflation mandate of 2% decided by some dudes in suits.

The cost of EVERYTHING is falling when you price it in bitcoin. EVERYTHING. Don’t focus on the number of bitcoin you have, focus on its purchasing power.

A deflationary/disinflationary money for a world dominated by technological advancements that are inherently deflationary. Perfect symbiosis.

SEC is going after Coinbase, Binance, and Crypto

I don’t know what the end result of this will be, maybe nothing but a fine, maybe much, much more. This is the risk with altcoin cryptocurrencies right now, as I’ve been saying all along.

They are SUPER speculative and super risky. 99.5% have no real use case and are just scams/gambling tokens ($doge, $pepe, $shiba). The SEC is on a mission to label these tokens as securities, and with that will come major headaches for the token issuers in the United States. The SEC believes they are unregistered securities in their current state and are systematically attacking them to bring them into compliance (which would likely ruin the cryptocurrency and its value).

Interestingly, Ethereum was not named in the filing, but it may just be a matter of time. Ethereum is highly centralized with a core group that controls the monetary policy to their benefit, and now uses staking after transitioning from Proof of Work to enrich early incumbents with more tokens created out of thin air as “yield”. I’m highly skeptical of ETH’s future and the purpose it will serve, and how it will differentiate and sustain itself from the competition over time. I lack conviction compared to bitcoin, but I still think ETH will do well in the next bull run, just FYI.

Bitcoin, on the other hand, you will never see named in a lawsuit because there’s no one to sue. Who are you going to charge, Satoshi? It’s a fully decentralized network that no one owns or controls and has a fixed monetary policy from day 1. It’s a commodity, like oil or gold, just digital. The first of its kind, and it can never be recreated (like fire). The SEC acknowledges this and you can rest easy. All those billions and billions of dollars in other cryptocurrencies are likely to flow into bitcoin at some point as people realize gambling on a dog token is probably not smart. I’ll be patiently waiting, doing what I always do.

And the show goes on!

Until next time…

Thanks for reading!

THIS is Crypto Pulse